Chapter 3: Tax Regimes in the Petroleum Sector

There are three main factors that define the economic value of a state’s oil resources (Figure 21). These are:

-

the exploitability, which is linked to the quantity of petroleum resources discovered and the geological and technical conditions necessary for their development;

-

market conditions that are defined by the price of crude oil on the international market; and

-

the tax regime, which is the regulatory framework developed by the State and which defines the tools for managing petroleum resources.

Figure 21: Economic Value of Hydrocarbon Resources

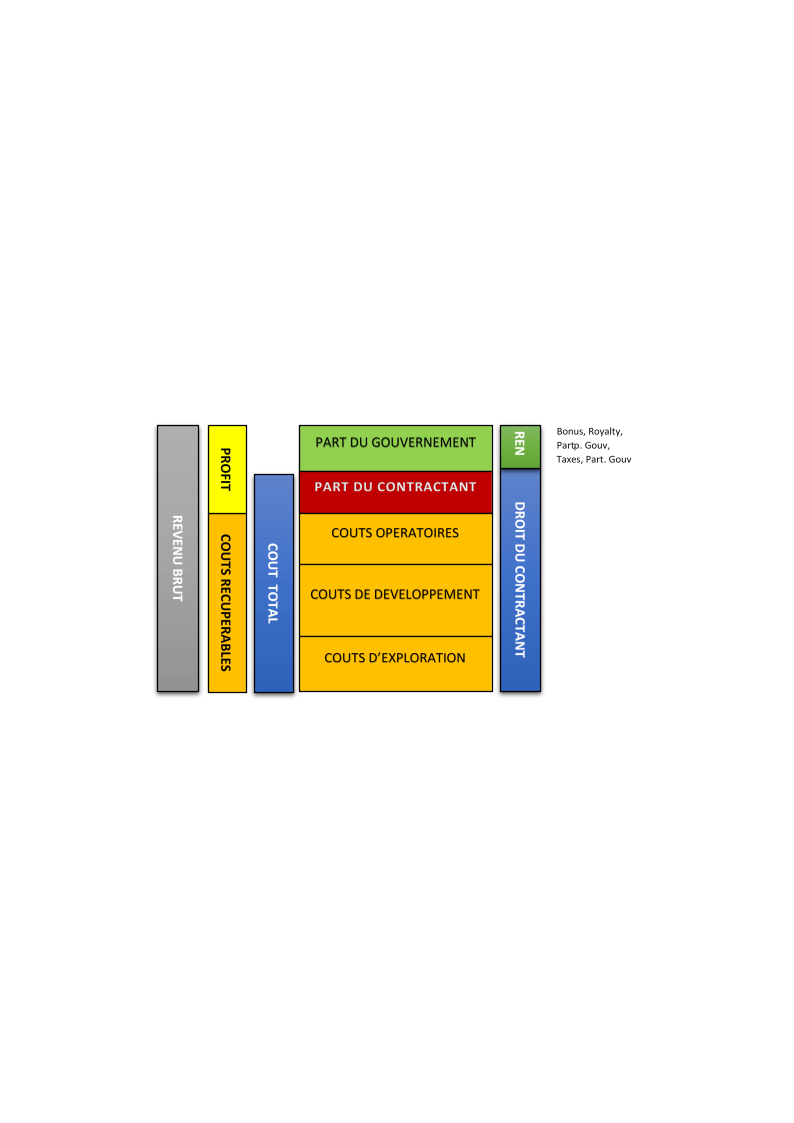

The economic income of an oil-producing state is the benefit that this state derives from the development of its oil resources (Figure 22). It is calculated by subtracting from the total monetary value of hydrocarbons in the subsoil, the various investments for its development, from exploration to abandonment, including exploitation, and the share of the profits accruing to the investor. For the State, which owns the resources, it is equivalent to the share or fraction that is due to it, and which is collected through a certain number of mechanisms, namely, bonuses, royalties, dividends from the direct participation of the State, its share of the oil profit and taxes.

The remaining oil after deduction of investment (profit), called oil profit, is shared between the government (state) and the contractor in accordance with the tax regime on the basis of which both parties have committed themselves through the oil contract.

The obvious and sometimes contradictory interests of the State and the Contractor (CPI) noted during the negotiation of contracts are linked to the degree of risk-taking by the parties.

Indeed, the CPIs that take huge amounts aim: i) the profitability of the project, ii) better profits for the shareholders and consequently iii) a large production at a high plateau in a relatively short period of time in order to recover their investments as quickly as possible, i.e. to have a quick return on investment. These are the financial risks linked to the heavy investments required for oil exploration, the political risks that can arise in the event of political instability (wars, change of political regime, etc.), the economic risks linked to the change in the tax regime and/or the drastic drop in the price of a barrel of oil on the international market, and geological and technical risks.

On the other hand, the State’s objective is to ensure from its oil resources: i) long-term benefits for its population, ii) employment, well-being, the transfer of skills and by extension iii) the exploitation of resources for the longest period of time with the highest possible recovery rate.

Figure 22: Distribution of income from production (After Johnson, 1995)

REVENUE BREAKDOWN

3.1- Tax system or system: Conceptual foundations

The tax system is the most important resource management tool for states. This is why it is mandatory for all managers and decision-makers in the oil sector to understand the basic principles, types, advantages and disadvantages of each tax regime.

The main objective of oil taxation is to capture economic rent, i.e. the surplus remaining after deduction of costs and a reasonable return on investment. Institutions such as the World Bank and the IMF generally insist that governments must secure a fair share of this rent, while leaving investors with sufficient earning potential to justify the risks involved.

Oil projects require significant investment and span the long term, often several decades. As a result, tax systems must take uncertainty into account. One of the key principles is progressivity: the state’s share must increase with profitability. This ensures the viability of projects in times of low prices, while allowing the government to benefit more when economic conditions improve.

At the same time, investors need stability. Sudden or unpredictable budget changes can undermine confidence and delay investment decisions.

Governments, on the other hand, need flexibility to adapt to changing economic conditions. Striking the right balance between stability and adaptability remains one of the key challenges in designing and adopting effective oil tax systems.

There are two families of tax systems in the oil industry, namely concession systems and contractual systems (Figure 23). The laws or regulations applied to oil exploration and exploitation in a country depend on the tax regime adopted by that country.

Figure 23: Classification of tax regimes

-

Argentina

-

Brazil

-

Venezuela

-

Philippines…

3.2- The concession system

The concession known as a license or lease is the oldest and most widely used of the tax regimes for petroleum agreements. This system is most often characterized by agreements based on Royalties and Taxes. This system has the following characteristics:

-

The oil company has the exclusive right to explore and produce at its own risk and expense;

-

The oil company owns the production;

-

The oil company pays the ad valorem royalty and the surface royalty to the State;

-

The oil company pays taxes on profits;

-

The oil company has the right to export hydrocarbons;

-

The oil company holds title to the equipment.

3.3- The contractual system:

In this system, there are two categories or types of contracts, namely the Production Sharing Contract (PPC) and the Service Contracts.

- The Production Sharing Contract (PPC)

The Production Sharing Contract ( PSC ) is the most commonly signed type of oil contract in Africa and is based fundamentally on three cardinal elements, namely: recoverable costs, oil profit sharing between the Government and the ICC and taxes on profits.

It was experimented with more the first time in Indonesia. In general or standard terms, a CPP contains provisions on the following elements:

-

Bonuses: these are signing, discovery or production bonuses. It is a lump sum paid under the conditions and within the time limit provided for by the regulations by the contractor, who holds an exploration or exploitation permit, but which is generally non-refundable, i.e. this amount paid is not included in the recoverable oil costs.

-

Work obligations: this provision defines the volume of work that will be carried out by the contractor during the contractual period. It is generally a question of quantifying the volume of 2D and/or 3D seismic and other Geological and Geophysical (G&G) studies to be carried out, the number and type of wells to be drilled with the related projected expenses

-

Royalties: these include:

-

the royalty, also known as the ad valorem royalty, which allows the states that own the resources to dispose of part of their resource before any sharing of oil and profit; and

-

surface royalties, which are rights to lease the block or perimeter under contract;

-

Cost oil: this section defines and clarifies the operations, activities or fees paid or spent by the contactor and which will be reimbursed in the event of discovery during the production phase in accordance with the terms and conditions set out in the CPP;

-

Profit-sharing of oil : in a CPP, the terms and conditions for sharing oil-profit between the parties (contracting party and State) must be known with previously defined distribution keys;

-

State participation: This is a share of action granted to the State and which is defined in the CPPs. The terms and conditions of the State’s participation as well as the rate of this participation in oil exploration and exploitation operations are specified in the contract. Generally, for many countries, the State’s participation is carried out in the exploration and development phase;

-

Domestic market obligations: the rules for selling hydrocarbons to the State at a preferential price solely for the satisfaction of the country’s needs must be defined in the CPP. It allows States to ensure their energy security through the exploitation of their resources. This obligation governs the export of petroleum resources by the ICCs, especially when the country’s domestic needs are not yet met.

-

The employment and training of local staff: this provision is very important to the point that it has now been extended to encourage the takeover of a certain number of activities by local staff and companies. The aim is to develop Local Content, a concept currently used to promote the establishment of local services and the development of national companies in the oil sector with a view to an efficient and operational transfer of technology and knowledge. In view of the importance of Local Content, some States have established it as a law or special regulation.

The essential characteristics of a PPC are:

-

the contractor shares the risks with the State;

-

the contracting party obtains a share of the production, generally in kind;

-

the State holds the title to the equipment;

-

the State retains its title to the oil. In other words, the contractor never holds title to the oil

- Service Contracts

Service contracts can be divided into pure service contracts and risky service contracts.

- Pure Service Contras

In this category of contracts, the state takes all the risks and hires an oil company to explore and produce oil discoveries for remuneration that is independent of or does not take into account the profit of the project. Such contracts exist in the Middle East but are rare in other parts of the world. It is this type of contract that Benin signed in 1979 with the Norwegian company SAGA Petroleum for the development of the Sèmè field. Similar arrangements are used by oil companies towards service companies such as PGS, Schlumberger and others.

- Risky Service Contract

Risky service contracts involve the oil company taking a risk and are the most commonly used service contracts.

In the case of this type of contract:

-

the contractor shares the risk with the State;

-

the contracting party receives a share of the profits, usually in cash;

-

The State holds title to the equipment and retains its title to the oil;

-

The contractor never holds title to the oil.

Risky service contracts are in many ways similar to production sharing contracts, except for the method of payment (cash or in-kind) and the same elements and mechanisms are used to regulate the relationship between the two parties in these two types of contracts.

- Structure of Oil Tax Systems in West Africa

Most tax systems in West Africa are based on a combination of instruments, each serving a specific function. Royalties generate quick revenues, but can be regressive, especially for marginal deposits. Cost-recovery mechanisms, particularly under production-sharing contracts, allow investors to recoup their expenses, although these mechanisms are usually capped to ensure that the government begins to collect oil profits within a reasonable period of time.

Taxes on profits, such as corporation tax or capital gains tax, are the main instruments for capturing economic rent and introducing progressivity. Premiums are initial payments, but generally contribute less significantly to overall revenues. State participation, most often through national oil companies, can strengthen public control and returns, but also exposes the State to financial and operational risks.

It is the interaction between these elements, rather than a single component, that determines the overall share of government and influences how investors assess risks and rewards.

- Contractual frameworks in West Africa

Production sharing contracts (PSCs) are the dominant model in West Africa. They allow governments to retain ownership of resources while relying on private companies to provide capital and technical expertise. Under a CPP, contractors assume the risks of exploration and development, recover their costs through production, and then share the remaining oil profits with the state.

Concession systems are still used in some states, particularly those influenced by Anglo-Saxon legal traditions or those with a more mature oil sector. Service contracts are less common, but exist in some special cases. In practice, many countries use hybrid approaches, combining elements of different systems to meet the specific needs of their projects or policy objectives.