Exploration and Exploitation of Petroleum Resources in West Africa

Welcome to the online reading edition of Exploration and Exploitation of Petroleum Resources in West Africa. This mdBook version converts the edited Word manuscript into a structured, searchable resource for students, researchers, policy makers, and energy-sector professionals.

Reading Guide

The book examines the petroleum value chain, upstream oil operations, fiscal regimes, governance risks, and country-level petroleum-sector analysis across West Africa.

Start with the Foreword, move through the General Introduction, or go directly to Chapter 1.

Source Note

This edition was generated from the edited Word manuscript and normalized for web reading with mdBook. Figures extracted from the manuscript are stored in src/images/ and referenced from chapter files using relative paths.

Front Matter

Preface

CONTENTS

FOREWORD

GENERAL INTRODUCTION

PART I: GENERAL INFORMATION ON THE OIL INDUSTRY AND THE CHALLENGES OF RESEARCH AND EXPLOITATION IN WEST AFRICA

Hydrocarbon sector value chain

Different phases of upstream oil and the roles of states

PART TWO: OIL CONTRACTS AND OIL TAXATION IN WEST AFRICA

Tax regimes in the oil sector

- Comparative study of tax regimes in selected West African countries

PART THREE: POLITICAL STABILITY, GOVERNANCE AND CORRUPTION IN THE OIL SECTOR

Key socio-political determinants of oil sector performance

West Africa – in-depth country analysis

GENERAL CONCLUSION

GLOSSARY

BIBLIOGRAPHICAL REFERENCES

List of Figures

Figure 1: Petroleum sector value chain 16

Figure 2: a and b Map showing the MSGBC Basin and Map showing the basins of the northern part of the Gulf of Guinea in West Africa 20

Figure 3: Map showing the sedimentary basins of Mali and Niger 20

Figure 4: Synthetic diagram showing the different oil cuts 30

Figure 5: Different phases of upstream oil 32

Figure 6: Process for allocating oil blocks to the IPC for petroleum exploration and exploitation 35

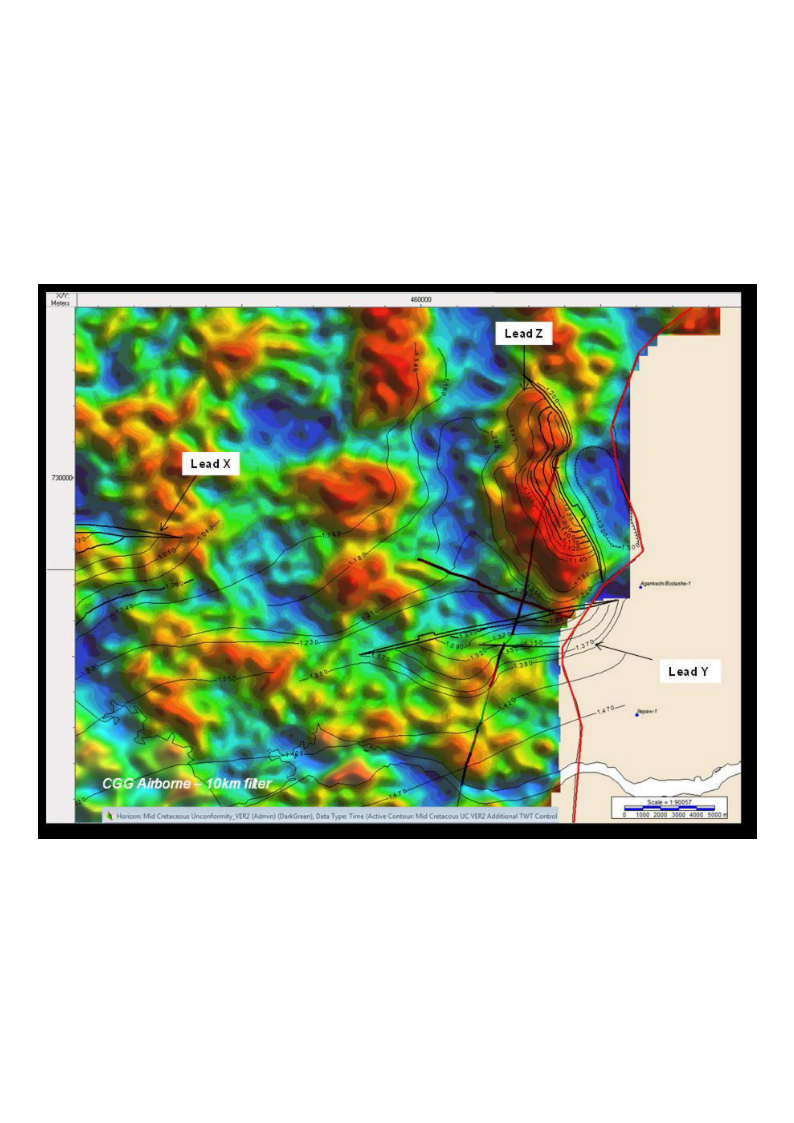

Figure 7: Gravimetric acquisition (a) showing anomalies in the Coastal Sedimentary Basin of Benin (CGG 2013) and aeromagnetic (b) to characterize the basement and sedimentary formations 37

Figure 8: 3D acquisition principle (a) and seismic cube (b) 38

Figure 9: Seismic amplitude anomalies showing Brightspots and Flatspots 38

Figure 10: Electromagnetism coupled with seismic reflection showing the resistivity contrast at the traps highlighted by seismic 39

Figure 11: Geological section showing the stratigraphic extent of the fictitious Deer-Boar oil system at the critical time (250 Ma). The thermally immature source rock is above the oil window. The active source rock is down-dip of the oil window (Magoon and Dow 1994) 40

Figure 12: Geoseismic section showing petroleum systems in the Benin Coastal Sedimentary Basin, Kerr McGee, 2003 41

Figure 13: Seismic interpretation showing a structural trap (anticline) 42

Figure 14: Some types of traps 42

Figure 15: Depth map showing the roof of a tank 43

Figure 16: Photos showing the core library of Côte d’Ivoire at the Directorate of the PETROCI Analysis and Research Center 47

Figure 17: Methodology Tank Evaluation 50

Figure 18: Diagram showing a reservoir model (Vilgeir Dalen, StatoilHydro, 2007) 51

Figure 19: Oil field production profile showing the life cycle of an oil field 55

Figure 20: Cash flows during the different phases of upstream oil activities (Dr. Alfred Kjemperud, 2007) 62

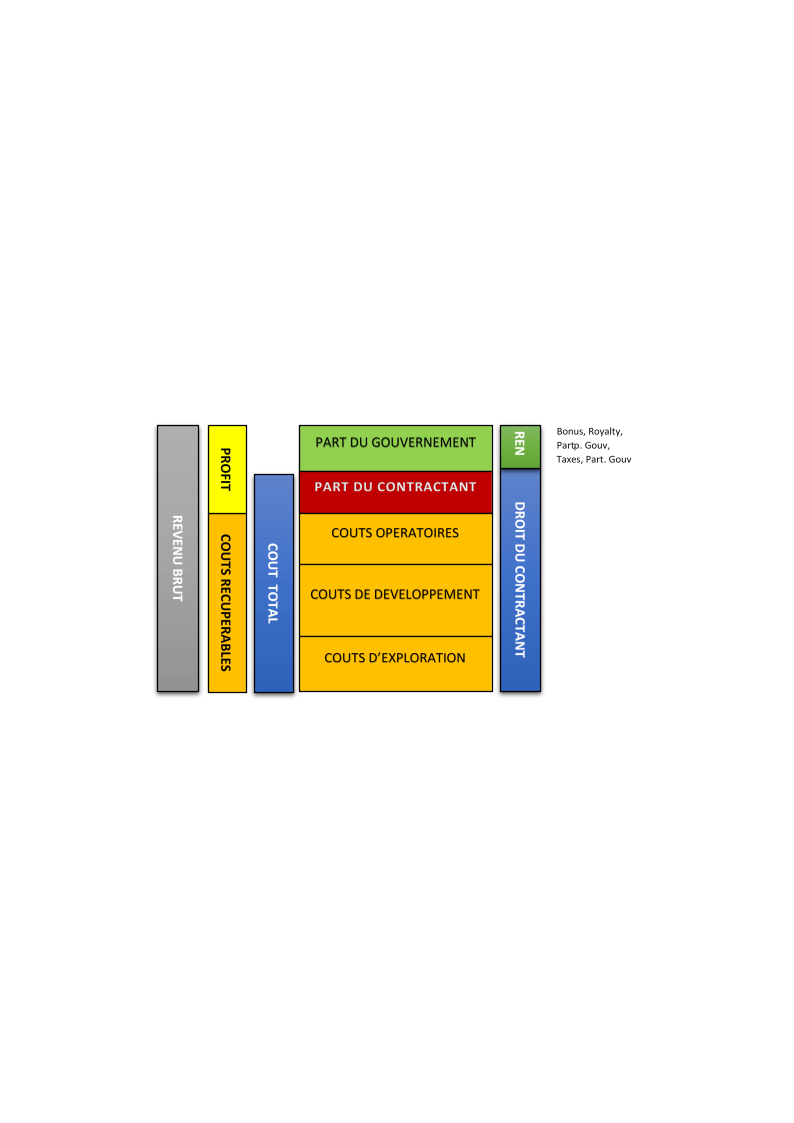

Figure 21: Economic Value of Hydrocarbon Resources 65

Figure 22: Distribution of income from production (After Johnson, 1995) 66

Figure 23: Classification of tax systems 67

Figure 24: Graph showing the cost stops applied in selected West African countries 75

Figure 25: Simplified organizational chart showing the share of the State and the Contractor in the taxation associated with the CPP of Benin 85

Figure 26: Simplified Organizational Chart Showing the State and Contractor’s Share of the Taxation Used in Ghana’s Model Contract 86

Figure 27: Simplified organizational chart showing the share of the State and the contractor resulting from the taxation associated with the CPP of Côte d’Ivoire 87

Figure 28: Simplified organizational chart showing the share of the State and the Contractor in the taxation associated with the CPP of Nigeria 88

Figure 29: Simplified organizational chart showing the share of the State and the Contractor resulting from the taxation associated with the Senegalese CPP 89

Figure 30: Simplified diagram showing the share of the State and the Contractor resulting from the taxation associated with the CPP of Niger 90

Figure 31: Graph showing the share of net profit accruing to the CPI and the States according to the tax regime applicable in these States 92

Figure 32: Graph showing the distribution of the cash flow between the government and the contractor considering 100 barrels of oil extracted 92

List of Tables

Table 1: Estimation of hydrocarbon resources in West Africa 17

Table 2: Daily output of countries (Trading Economics, 2025) 18

Table 3: Type of crude oil in selected West African countries 21

Table 4: Calculation of financial losses resulting from a measurement error of 0.4 % 58

Table 5: Summary of ad valorem royalty rates applied in selected West African countries 73

Table 6: Oil-profit sharing mechanisms in selected West African countries 78

Table 7: Profit tax rates applied in selected West African countries in the oil sector 80

Table 8: State participation rates in selected West African countries 81

Table 9: Summary of the key tax terms for determining the share of the parties’ overall cash flows for oil 83

Table 10: Distribution of the net revenues (share) of the State and the Contractor arising from the tax regimes of the petroleum laws and regulations of the countries studied 91

Table 11: Cash flow representing the share of each part per 100 barrels of oil produced 91

Abbreviations, Acronyms and Abbreviations

ABEX : Abandon Expenditures

AFREC: African Energy Commission

IEA: International Energy Agency

APPO: Organization of African Petroleum Producers

AVO : Amplitude Variation with Offset

API : American Petroleum Institute

BBL/D/1K: One Thousand Barrels Per Day

BCF: Billion cubic feet

CAPEX : Capital Expenditures

ECOWAS: Economic Community of West African States

CO2: Carbon Dioxide

CPI: International Oil Company

CPP: Production Sharing Contract

CNPC: China National Petroleum Corporation

UNCTAD: United Nations Conference on Trade and Development

DHI: Direct Hydrocarbons Indicator

DPB : Benin Oil Depot Company

DW: Deep Water

IMF: International Monetary Fund

GAO: West Africa Gas Pipeline

LNG: Liquefied Natural Gas

GNPC : Ghanean National Petroleum Company

LPG: Liquefied Petroleum Gas

EITI: Extractive Industries Transparency Initiative

MMBBLS: Million de barils

NNPC: Nigerian National Petroleum Company

NOx: x Nitrogen oxide

OPEX: Operating Expenditures

NATO : North Atlantic Treaty Organization

PDO: Development and Operation Plan

PETROCI: National Company of Petroleum Operations of Côte d’Ivoire

PETROSEN: Société Nationale des Pétroles du Sénégal

GDP: Gross Domestic Product

PPS: Sèmè Oil Project

PSA : Production Sharing Contract

SAPETRO: South Atlantic Petroleum

SAR: Société Africaine de Raffinage

SIR: Société Ivoirienne de Raffinage

SMB: Multinational Bitumen Company

SONANGOL : Société Nationale des Pétroles de l’Angola

SONATRACH: National Hydrocarbons Company of Algeria

SONIDEP: Nigerien Oil Company

SORAZ: Zinder Refining Company

SW : Shallow Water

TCF: Trillion Cubic Feet (1000 BCF)

TOR: Tema Oil Refinery

UDW: Ultra Deep Water

VSP: Vertical Seismic Profil

WAPCo: West African gaz Pipeline Company

WAPCO: West African Oil Pipeline Company

AfCFTA: African Continental Free Trade Area

Foreword

Geo-extractive resources are a source of income for countries that have them and occupy a large part of the Gross Domestic Product (GDP) of some countries. They have been the basis of the economic and industrial development of many countries. Petroleum resources (oil and natural gas) in particular are strategically important energy sources and played a prominent and decisive role during the Industrial Revolution in the 19th century. In addition to their interest for development, oil resources are also at the origin of environmental disasters, endogenous tensions and wars between certain states. This bipolar dimension or duality characterizing the use of this resource is linked to its multiple uses, which can be grouped into two groups:

Use for socio-economic development:

-

It is a universal medicine used since the 1st century AD: bitumen is prescribed against leprosy, cataracts, gout… It was used in Mesopotamia to cure dermatological ailments and also by the Egyptians and even in the thirteenth century in France.

-

It is the most widely used source of energy for industrial development: In the nineteenth century in Europe and the United States, oil was the driving force behind the development of industry and transport. Today, despite international policies to develop cleaner energy sources, including renewable energy, as well as strategies to limit or even eliminate the exploitation of fossil fuels, hydrocarbons remain the most widely used primary source of energy in the world.

Weapon of war and source of environmental pollution

-

Oil is also a weapon of war: it has been used in the Persian wars between Greece and Persia since the fifth century, as well as in the world wars where energy played a strategic role. For example, the control of Kuwait’s oil reserves by the US was the main cause of the Gulf War (1990-1991). The same is true of the Biafran war in Nigeria (May 1967-January 1970) maintained by France, and more recently in 2011, it was the real motives of the destabilization of Libya by the Western powers that are in particular France animated by the desire to control Libyan oil and to increase its influence in North Africa with the support of other NATO countries particularly the USA.

-

From an environmental point of view, the extraction of hydrocarbons and the use of petroleum products resulting from their transformation are at the origin of climate change because they emit greenhouse gases, which are responsible for global warming which causes severe weather and climate conditions, namely: the melting of glaciers, the rise in sea level, floods, drought etc.

In order to secure this valuable source of energy for industrial development, Westerners undertook oil exploration work in Africa during the 20th century. During the colonial period (before 1960) and especially in the early years of the post-colonial period, the first works carried out by foreign powers made it possible to make the geological mapping of Africa. This mapping revealed that the African continent has a significant potential in geo-extractive resources, particularly oil and natural gas.

The development of oil resources requires the existence and mastery of technology, skills and financial resources that are not available to third world countries, particularly those in Africa. thus. To do this, African countries negotiate agreements with foreign powers whose terms and implementation are poorly controlled or controlled. On the other hand, responsible, sustainable and transparent management of oil revenues by governments is decisive in boosting socio-economic development in states. As a result, for more than three decades of exploitation of oil and gas resources in Africa, the profits they derive are insignificant due on the one hand to the signing of unbalanced contracts that are not very profitable to States and on the other hand poorly managed. This state of affairs is illustrated by three observations:

-

Most African countries that exploit oil resources live below poverty.

-

Half of Africa’s population does not have access to energy, even though it exports a large part of its hydrocarbon production (40% of gas and 50% of oil) in the form of raw materials, according to the International Energy Agency (IEA) in 2017.

-

the lack of appropriate infrastructure for the processing and development of the entire value chain of the oil industry.

The present work aims to lift a corner of the veil on the challenges of African States from the exploration to the exploitation of hydrocarbons, to analyze the tax regimes associated with oil legislation in certain West African countries and finally to highlight the fundamental levers on which States must act to maximize their profit and gradually reverse this unprofitable trend that characterizes the exploitation of oil resources in most countries. countries of West Africa.

This reflection also calls for the responsibility of African States in the monitoring and technical and sovereign control of oil operations in order to optimize their profit margin and ensure compliance with safety and environmental standards accepted in the international oil industry or governed by national legislation.

We believe that we have, through this book, given an overview of the oil sector and the difficulties and challenges related to the exploitation of resources for the benefit of the populations of West Africa, and made our contribution to the development of a real oil industry in West Africa.

This book owes a lot to some people who supported me in this exercise and who gladly made their contributions and constructive comments.

I would like to express my great gratitude to Mr. Matt …., Doctor of Geological Engineering and Independent Consultant in Petroleum Geosciences who did me honor by agreeing to write the preface to this book.

General Introduction

Formed underground between 20 and 350 million years ago, hydrocarbons (oil and natural gas) are and remain the most widely used primary energy source in the world, despite the emergence of renewable energies, which are now considered cleaner energies due to their low carbon footprints. They are a lever for development for nations because of the immensity of the products and by-products as well as the uses that result from the transformation of this raw material.

Over the years, the oil sector has become a real industry that has embraced for its development the engineering sciences (mechanics, electronics, physics, chemistry, mathematics, geology, etc.), legal, economic, political and also social sciences.

The negotiation of exploration and exploitation contracts and the management of oil conflicts require legal, geopolitical and diplomatic knowledge and skills.

The search for oil and its extraction require advanced and innovative technologies that have been developed over time and that are adapted to the geographical and geological environment in which it (oil) was formed.

The possibilities of its extraction and development (processing) are defined by researchers and engineers in petroleum geosciences (petroleum geology and geophysics, geochemistry, drilling, reservoirs), petroleum refining, petrochemicals and economics who carry out technical studies and evaluations of the economic and financial profitability of petroleum projects.

The main purpose of this reflection, which gives a global overview of the oil sector in West Africa, is to question the responsibilities and roles of States as well as to evaluate the benefits that the latter derive from this business vis-à-vis foreign investors from exploration to exploitation, so as to ensure that oil in Africa is no longer as Bruno Carton (2000) so aptly put it, “violence against peoples” or “rent (which) feeds rent and debt” but rather a pledge of peace and a source of prosperity.

This work, structured in three parts and six (6) chapters, deals with the various aspects and themes relating to the policy, governance and management of petroleum resources, as well as the strategy for the development of a viable, integrated and sustained petroleum industry in West Africa.

The first part is devoted to general information on the oil industry and the responsibilities of States in the monitoring and control of oil exploration and exploitation activities.

The second part deals with oil contracts and oil taxation and analyses the different tax regimes used in West Africa.

The third part examined the influence of political stability, governance and corruption on the performance of the oil sector in West Africa.

Specifically, the first chapter addresses the value chain of the hydrocarbon sector. The concepts developed in this chapter are intended for students of petroleum sciences but also for managers and decision-makers in the oil sector at the level of West African States. Mastery of these concepts will enable States to adopt policies and strategies based on the establishment of the necessary technical and infrastructural capacities at the level of all links in the oil chain, from upstream to downstream, in order to place on the market of the Community and world space finished products or, at the very least, semi-finished products resulting from the processing of hydrocarbons.

The second chapter devoted to upstream oil zooms in on oil exploration and exploitation strategies. This chapter thus develops the entire process and techniques that contribute to the allocation of permits as well as to the conduct of hydrocarbon exploration and exploitation operations. It is mainly aimed at students in petroleum geosciences.

The third chapter deals with tax regimes in the oil industry, a very essential theme for students of petroleum sciences but especially for managers and decision-makers in the hydrocarbon sector. The aspects discussed can serve as a guide or guidance in the context of the implementation of legislative and regulatory texts to govern the oil sector, particularly in its fiscal and economic aspects.

The fourth chapter uses the concepts developed in the second and third chapters to make a comparative study of the tax regimes used in six West African countries and to deduce the cash flow and revenues derived by each party (State and contractor) to the contract for the exploitation of petroleum resources.

The fifth chapter examined the socio-political determinants to ensure a good performance of the oil sector before identifying the roles of the various key actors, namely the State, operators or investors and international institutions to prevent political instability, bad governance and corruption in the sector. The topics discussed are useful for policymakers and all actors in the oil sector.

Finally, the sixth chapter provides an in-depth analysis of the situation of political stability, governance and transparency in the management of oil resources in some West African countries and their influence on attracting foreign investment and on the responsible management of oil rents for the benefit of the population.

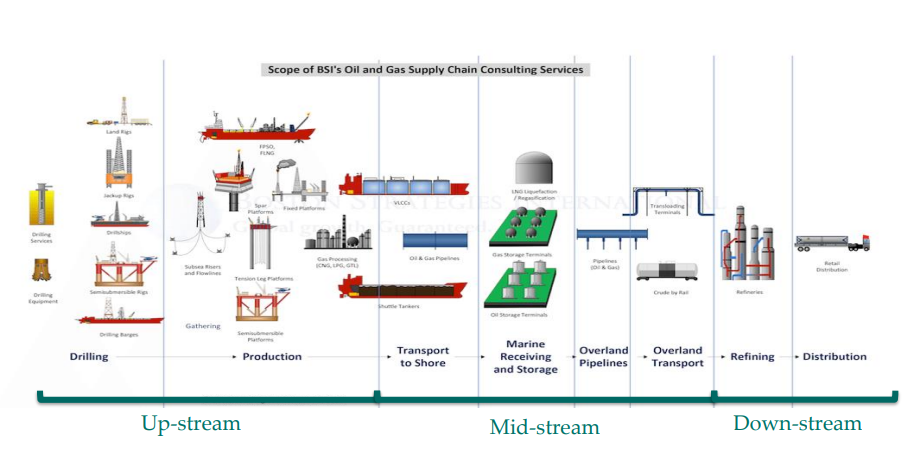

Chapter 1: Value Chain of the Hydrocarbon Sector

As shown in Figure 1, the value chain of the oil sector or the oil industry includes three segments, namely: upstream, midstream and downstream.

Figure 1: Oil Sector Value Chain

- The Upstream segment

1.1.1 - Features

Upstream oil is the foundation or early stages of development of the oil industry. It is characterized by a complex set of operations that contribute to the discovery and exploitation of oil and natural gas formed millions of years ago in the subsoil. The upstream segment essentially includes activities from the exploration to the production of hydrocarbons. It deals with the location of oil and gas extraction sites, exploration drilling and the production of crude oil and natural gas. Three main stages make up this segment:

-

Research or exploration: the identification of hydrocarbon accumulations by various geological and geophysical methods at the surface and depth following the granting of a petroleum licence or authorization;

-

Extraction or exploitation which is composed of two sub-phases:

-

Development: the determination and implementation of technical and infrastructural conditions for extraction according to geological, reservoir and economic parameters

-

The production of the field during which the various techniques of extraction and recovery of oil and natural gas are implemented;

-

-

Abandonment, which generally occurs when oil reserves are depleted and it is necessary to secure and/or dismantle production facilities and infrastructure to avoid and/or minimize various environmental problems inherent in the operation.

The fundamental characteristics of upstream segment operations are:

-

High geological risk, which results in high uncertainty or no guarantee of discovery of commercially exploitable reserves.

-

Colossal investments: exploration and development activities involve heavy capital investments due to the advanced technologies used, equipment and infrastructure necessary to carry out these operations;

-

the management of environmental and safety risks and impacts inherent in research (seismic, drilling, etc.) and production operations (pollution of terrestrial, marine and atmospheric environments by oil spills, flaring, gas leaks and emissions, fires and other construction site accidents).

1.1.2- State of play in West Africa

The West African sub-region holds a third of the continent’s oil and natural gas reserves . About 30% of the world’s oil reserves are in the Gulf of Guinea (ECOWAS, 2019). An assessment of hydrocarbon resources after recent discoveries in some West African countries estimates reserves at about 39 billion barrels of oil and 372,000 billion cubic feet (372 TCF) of natural gas (Table 1).

| Country | Crude Oil Reserves (MMBLS) | Gas Reserves (BCF) |

|---|---|---|

| Nigeria | 30.031* | 202.000* |

| Ghana | 1813 (732 proven) | 4,100 (1,771 proven) |

| Senegal | 2 030* | 42 024* |

| Mauritania | 20 (proven)* | 110 000 (estimation)* |

| Ivory Coast | 3.100 (estimation)* | 4.600 (estimation)* |

| Niger | 150 | |

| Benin | 331 (estimation) | 477 |

| Guinea-Biseau | 840 | |

| Mali | 645 (estimation)** | 9 000 (estimation)** |

| Total | 38 960 | 371 724 |

Table 1: Estimation of hydrocarbon resources in West Africa

*Data Ministries

**RPS Energy Report, 2006

According to Trading Economics (2025), the four (04) largest producers in 2024 (Table 2) are Nigeria (Benin Basin, Niger Delta and intracardboard basins) which is by far the most popular with 1,539,000 barrels/day, followed respectively by Ghana (Saltpond and Tano basins), 188,000 barrels/day, Niger (three intracratonic sedimentary basins, namely Chad, Illumenden, Djado), 53,000 barrels/day and Côte d’Ivoire (offshore coastal sedimentary basin), 47,000 barrels/day.

| Country | Last | Previous | Reference | Unit |

|---|---|---|---|---|

| Nigeria | 1539 | 1485 | 2025-01 | BBL/D/1K |

| Ghana | 188 | 188 | 2024-10 | BBL/D/1K |

| Niger | 53 | 43 | 2024-10 | BBL/D/1K |

| Ivory Coast | 47 | 42 | 2024-10 | BBL/D/1K |

Table 2: Daily production of countries (Trading Economics, 2025)

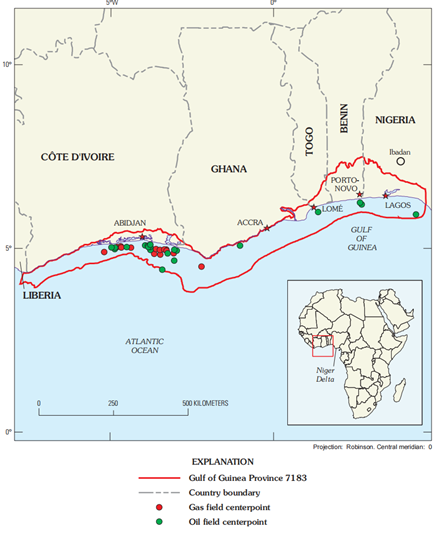

Significant discoveries of oil and especially gas have been made onshore and offshore in Senegal and Mauritania in the Senegalese and Mauritanian sedimentary basins that are part of a vast West African Basin called “MSGBC Basin (Mauritania – Senegal – Gambia – Bissau – Conakry)”, Fig. 2a. These two states, already oil producers, have started production of a large cross-border gas field thanks to the “Greater Tortue Ahmeyim” offshore gas project, whose resource discovered in 2015 by the American Kosmos Energy is estimated at more than 15,000 billion cubic feet. The field is being developed and produced with the support of the international oil company BP, with the entry of the first LNG cargo on the world market in April 2025.

Benin, located in the Gulf of Guinea, a proven oil-producing province (Fig. 2b), was also a producer from 1982 to 1998 of a marginal field located on Block 1 of its Coastal Sedimentary Basin, discovered in 1968 by the American company Union Oil of California. It has just restarted production from the Sèmè field with Akrake Petroleum, a subsidiary of the Norwegian company Rex, and has relaunched oil exploration.

Other countries are still in the exploration phase and will be able to make commercial discoveries in the sense that they are located in geologically promising areas. These include:

-

The Gambia, Guinea Bissau and Guinea Conakry, which share the same large MSGBC basin as Senegal, have good prospects for commercial discoveries given that the work carried out has proven the presence of hydrocarbons in their coastal basins. The same is true for Sierra Leone and Liberia, which are located in the same geological environment and whose coastal basins are framed by the large MSGBC basin and the Côte d’Ivoire basin in the Gulf of Guinea, where several discoveries have been made.

-

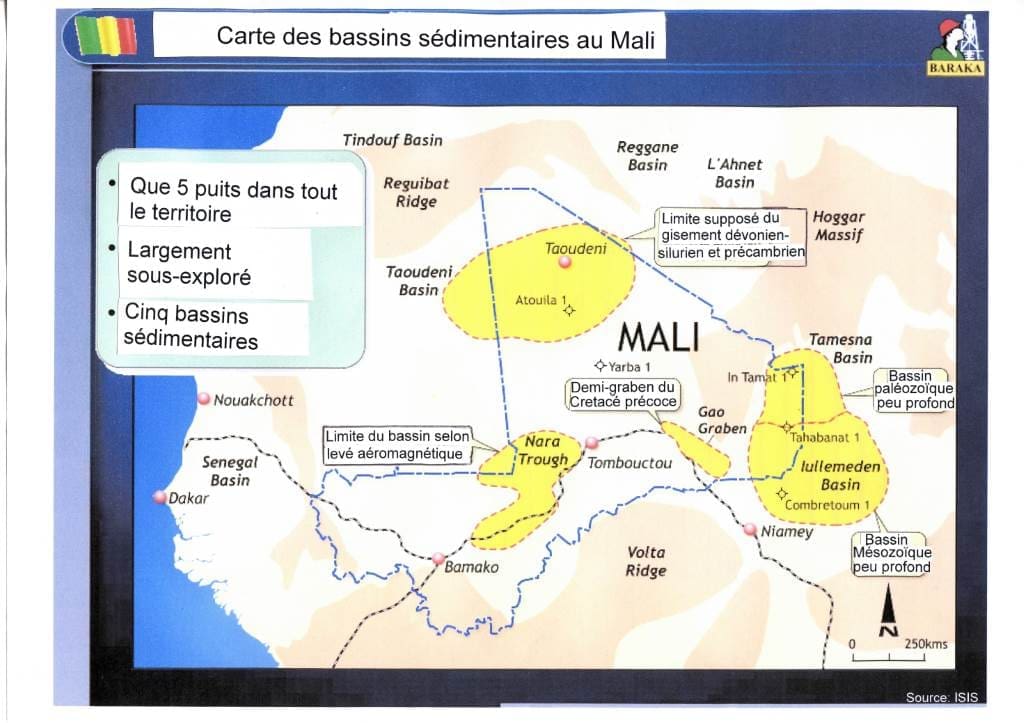

Mali with the Taoudéni Basin, the Nara Rift, the Gao Graben and the Tamesna Basin, which is the extension of the Ilullemedens Basin in Niger (Fig.3). Already in 2006, RPS Energy showed that the five blocks owned by the company Baraka Petroleum in the Taoudéni basin could house up to 645 million barrels of oil and 9 Tcf of natural gas.

-

Burkina Faso in view of its proximity to Mali and because of the presence of hydrocarbon showings identified in its western basin which borders the Nara basin in Mali

-

Togo whose coastal sedimentary basin is an integral part of the Gulf of Guinea, an oil-rich province proven by discoveries in Nigeria and Benin, Ghana and Côte d’Ivoire.

Figure 2: a and b Map showing the MSGBC Basin and Map showing the basins of the northern part of the Gulf of Guinea in West Africa

Figure 3: Map showing the sedimentary basins of Mali and Niger

Crudes discovered and produced in some West African countries are light to heavy with a low sulfur content (sweet) as mentioned in Table 3 below.

Table 3: Type of crude oil in selected West African countries

| Country | Density °API | Sulphur content (%) | Quality |

|---|---|---|---|

| Benin | 22 (Champ de Sèmè) | 0.32 | Medium and Sweet |

| 42 (Deep Offshore Block) | 0,1 | Light and Sweet | |

| Niger | 30 | Very Low | Medium and Sweet |

| Nigeria (Niger Delta Crude) | 20 to 25 |

0.17% Egina 0.6% (Qua Iboe et Forcados) |

Heavy, Medium and Sweet |

| 36 | Light and Sweet | ||

| Ivory Coast | 28, 31, 48 | Medium, Light and Sweet | |

| Ghana | 35,1 (Saltpont) | 0.16 | Light and Sweet |

| 35 (Jubelee) | 0.23 | Light and Sweet |

Some examples of internationally known upstream companies are ExxonMobil, Chevron, BP, Shell, ConocoPhillips, ENI, Total Energies, SINOPEC… These majors are joined by other independent oil companies that are challenging and investing in West Africa, such as Tullow in Ghana, Cairn in Senegal, Kosmos in Mauritania, CONOIL in Nigeria, CNPC in Niger, etc. In Africa, there is an emergence of National Hydrocarbon Companies such as SONATRACH in Algeria, PETROCI in Côte d’Ivoire, NNPC in Nigeria, SONAGOL in Angola, PETROSEN in Senegal, SONIDEP in Niger, GNPC in Ghana… but also some small private companies such as SAPETRO, ORANTO in Nigeria….

1.1.3- Main challenges

Faced with the issue of climate change, the challenges related to the financing of upstream activities, the development or the appropriation of technology remain a bone in the throat of African States and to which States must cooperate and pool their efforts in order to put in place appropriate strategies for the responsible and sustainable exploitation of their hydrocarbon resources.

- The midstream segment

1.2.1- Characteristics

The midstream segment of the oil and gas industry connects upstream and downstream oil activities and includes natural gas liquefaction and regasification operations, natural gas storage and transportation, and transportation of crude oil to refineries by means of ships, pipelines, tanker trucks, etc.

In detail, the intermediate segment includes activities related to:

-

the construction of oil and gas pipelines, crude oil and natural gas storage tanks, oil and gas loading terminals, and natural gas liquefaction and regasification facilities, including:

-

Flootload Liquefied Natural Gas (FLNG) units

-

Floating Storage and Regasification Units (FSRUs)

-

-

the transport of hydrocarbons by pipelines (oil and gas pipelines, etc.)

-

to the treatment of natural gas by separating it from the various hydrocarbons and fluids to produce a “pipeline quality” gas. In some cases, this activity may be considered to be an upstream oil activity

Crude oil and natural gas are transported either by land or by sea. The means of transportation typically used are tankers and pipelines that bring crude oil to refineries where it will be processed into petroleum products.

The term midstream is much more used in the oil industry in the US and Canada, which have developed large oil and gas pipelines and storage facilities run by private companies in these countries. For example, the Keystone Pipeline System is a network of oil pipelines in Canada and the United States, owned by TransCanada Corporation.

In European countries, the transportation and storage of crude oil tends to be integrated into upstream production activity. Many European pipelines are controlled by the governments of the countries they pass through or by state-owned crude oil transport companies in these countries. This state ownership tends to result in the absence of the midstream as a separately designated part of the oil production value chain.

Some examples of purely mid-market operating companies are Oasis Midstream Partners, Sanchez Midstream Partners, Hess Midstream, Magellan Midstream Partners, and EQT Midstream Partners. TransCanada Corporation.

1.2.2- State of play in West Africa

In West Africa, the transport network by gas and oil pipelines is still very weak. However, it should be noted that States are aware of the situation and that they are willing to develop structuring projects to secure the supply of hydrocarbons to the West African area.

The West African Gas Pipeline (WAG) and the Niger-Benin Export Pipeline are good examples of midstream development projects in this West African region.

The West African Gas Pipeline (WAG) is a natural gas pipeline transport system (onshore and offshore), over approximately 688.6 km from Nigeria (Alagbado) to Ghana (Takoradi) via Benin (Cotonou) and Togo (Lomé). Its objective is to transport natural gas produced in large quantities from Nigeria’s oil fields to Benin, Togo and Ghana, mainly for the production of electricity and the needs of the industrial sector. This pipeline, managed by the West African Gas Pipeline Company (WAPCo), has been operational since 2011 and aims to increase the population’s access to electrical energy at a reasonable cost and consequently give a boost to the economic development of states.

The Niger-Benin Export Pipeline is a pipeline transport system to export crude oil from AGADEM’s fields located in the DIFFA region of Niger via Benin through a loading terminal located at sea. This pipeline was built and is managed by the Chinese company WAPCO. It is the longest in the sub-region, has a length of 1,950 km, of which 675 km is on Beninese territory, and has a transport capacity of 90,000 barrels/day, extendable up to 140,000 barrels depending on discoveries in Niger.

In addition to these cross-border infrastructures, there are national oil and gas pipeline transport networks and crude oil storage infrastructures which are more or less developed in some countries such as Nigeria, Côte d’Ivoire, etc.

1.2.3- Main challenges

Challenges in the midstream sector include, among others, maintaining the integrity of storage and transport infrastructure (ships, trucks, wagons, pipelines, etc.), protecting workers involved in cleaning, purging and filling activities, and the lack of oil infrastructure to ensure the energy security of states.

In West Africa, the issue of securing infrastructure is worrying and topical. Security challenges are manifested by:

-

the vandalism of infrastructure due to the failure to take into account the socio-political realities and misery of the populations of the localities in which these sensitive and dangerous infrastructures are built;

-

acts of sabotage of facilities recorded by the growing rise of terrorism

To this end, the monitoring of these infrastructures and the real consideration of the concerns of indigenous populations must be considered more seriously in the context of oil and gas development projects. Taking these aspects into account will ensure the safety of workers and machines and avoid the risks of vandalism and sabotage of infrastructure that are the cause of oil spills, fires and explosions and consequently marine and terrestrial pollution.

The inadequacy and poor management of national and regional oil infrastructure for the transport and storage of hydrocarbons, liquefaction, regasification and gas processing is also a major weakness of the oil sector in West Africa.

The strengthening or construction of energy infrastructure such as gas-fired power plants and the creation of an African oil market will boost the development of the midstream and, in turn, strengthen people’s access to clean energy.

- Le segment Aval (downstream)

1.3.1- Characteristics

This segment deals with crude oil refining, transportation, storage and distribution of petroleum products as well as petrochemical activities. This is the stage where crude oil is transformed into different petroleum products namely fuel oil, diesel, gasoline (naphtha), kerosene (jet A1) and Liquefied Petroleum Gas (LPG) which are used for various purposes, such as powering vehicles, heating homes, electricity production etc. and asphalt or bitumen for road construction (Figure 4). The crude oil refining process is generally divided into three basic stages: separation, conversion, and processing. Refining techniques depend on the type of crude oil to be processed and the needs of the market. There are several types of crude oil classified mainly according to three criteria: density, sulphur content and geographical origin**.** API low-density and low-sulfur crudes have the best advantages because they are lightweight and less complex to refine and require little or no desulfurization.

In the petrochemical industry, long-chain hydrocarbons in oil and natural gas and naphtha are used to manufacture products such as plastics, rubbers and synthetic fibres, fertilizers, preservatives and detergents. For example, petroleum and natural gas products are used to make artificial limbs, hearing aids, and flame-retardant clothing to protect firefighters. Similarly, paints, dyes, fibers, etc. are made from oil and natural gas.

1.3.2- State of play in West Africa

In West Africa, the performance and quantity of refining units and infrastructure for the storage and transport of petroleum products remain problematic in that they are insufficient to cover fuel needs and ensure the security of supply of petroleum products. Thus, despite its great oil potential and the significant amount of oil production, most West African producing countries remain dependent on Europe and the Middle East for their supply of petroleum products, which constitutes an exorbitant bill for public finances.

This analysis is also confirmed by a study carried out in 2019 by ECOWAS on “the development of a regional programme on the facilitation of the supply of petroleum products”. The study found that: “The supply of petroleum products is highly dependent on external sources, resulting in a 70/30 import/local production ratio that does not guarantee security. The available refining capacity theoretically makes it possible to cover the demand for refined products… Unfortunately, the refineries are underutilized. They are only at 30% of their production capacity due to the obsolescence of poorly maintained equipment.”

In addition, the use of low-quality petroleum products is responsible for the emission of air pollutants such as carbon monoxides, benzenes, unburned hydrocarbons, particulate matter, nitrogen oxides, etc., which dangerously compromise human health, engine efficiency and the environment. Unfortunately, there is a large deviation from the specifications of petroleum products in Europe and West Africa. European standards have a sulphur content of 10 ppm for petrol and diesel oil, while almost all West African countries import or produce these products through their refineries with a sulphur content of 50 and 10,000 ppm for diesel and 50 and 3500 ppm for petrol, with the exception of Ghana and Benin, which have adopted better specifications in their legislation.pursuant to Directive C/DIR.1/9/2020 on harmonized specifications for automotive fuels (petrol and diesel) in the ECOWAS region. Bringing refineries in West Africa up to standard is becoming an imperative but requires huge investments that governments and their partners must face.

The actors in the supply and distribution of products in West Africa are made up of state companies or institutions, mixed companies, private and international. In addition to state-owned companies such as PETROCI and GESTOCI of Côte d’Ivoire, NNPC of Nigeria, PETROSEN in Senegal, GNPC in Ghana, DPB in Benin, SONIDEP in Niger, international traders such as Oryx, PUMA/Trafigura, Vitol and African traders such as La Chorale in Côte d’Ivoire, Sahara Group in Nigeria, ITOC in Senegal and private national storage and distribution companies such as Octagone, JNP, Benin Petro in Benin, BOST and GOCIL in Ghana…

As far as the refining industry is concerned, there are very few private companies in West Africa (the new DANGOTE refining company in Lekki, Nigeria, with an optimal capacity of 650,000 barrels per day, and a few state-owned or mixed refineries such as SIR/SMB in Côte d’Ivoire, SAR in Senegal, the NNPC refineries (Kaduna, Port Harcourt and Warri) in Nigeria, SORAZ in Niger, TOR in Tema in Ghana.

1.3.3- Main Challenges

In short, Africa in general is facing two major challenges in the downstream oil sector, namely:

-

the weakness of the security of supply of petroleum products, which limits access to energy and, in turn, is a brake on economic development, particularly in most countries of sub-Saharan Africa. This situation is linked to a lack of storage and distribution infrastructure and also to the weakness of the operational capacity for oil refining.

-

the poor quality of imported petroleum products and those from African refineries that do not meet international standards, with the exception of the new DANGOTE refinery in Nigeria.

- Weaknesses in the West African oil industry value chain

The value chain of the oil industry is not structured in Africa in general and in West Africa in particular. The oil sector faces challenges due to a lack of a coherent and operational regional organizational policy, a lack of synergy between the different segments of the oil industry, and the lack of a genuine African oil market serving Africans. The upstream oil sector is therefore characterized by a massive export of oil and gas resources produced to Europe and Asia in raw form and an import of refined and finished products. As a result, the oil sector is still subject to the dictates of foreign powers marked by:

-

A massive export of crude oil at a market price over which Africa has no control;

-

A steep and bitter bill for importing refined products and derivatives from their crude oil at a price whose setting mechanism escapes Africans.

In addition, the poor management of revenues from resource exploitation is also an obstacle to the endogenous financing of structuring development projects in Africa. It is important to draw the attention of States to the responsible management of revenues from the exploitation of oil and gas resources, given that most of Africa’s producing States are confronted with the “Dutch disease”, characterized above all by deindustrialization and their economic dependence on oil rents.

Indeed, the revenues derived from the exploitation of oil and natural gas, non-renewable extractive resources, should be directed and invested in the diversification of the economy with a view to the emergence of other viable economic and industrial sectors that make it possible to sustainably support the development of States.

Unfortunately, many African countries have economies that remain very fragile because they rely mainly on oil and natural gas production. In 2024, Libya is in the lead, with an impressive 56% of its GDP coming from oil rents, followed by Congo with 34% and Angola with 28%. Nigeria’s contribution to reported GDP of about 6% while more than 90% of its total export revenues came from oil shows a disparity between the direct contribution to GDP and the preponderance in export earnings and public finances. This situation reveals that Nigeria remains inherently dependent on oil and gas for its essential foreign exchange inflows and national budget.

The diversification of the economy is a major approach to avoid the risks of economic fragility linked to total dependence on oil resources, which are suffering the full force of the threats of oil counter-shocks, endogenous and exogenous geopolitical tensions, etc., but also of their certain depletion.

African regional institutions such as ECOWAS through its specific bodies and sectoral commissions, AFREC and APPO have a key role to play in establishing a link between the different segments of the industry in order to develop an integrated value chain for the optimization and generation of economies of scale to contribute to the industrialization and diversification of energy sources in the region.

1.4.1- At the ECOWAS level

In West Africa, the issue of pooling efforts and genuine cooperation for the development of an oil industry remains a challenge despite some ongoing actions. ECOWAS should be a springboard for the realization of these actions. The results obtained by this West African organization are not yet up to expectations. One of the flagship projects carried out by ECOWAS is the construction of the West African Gas Pipeline (WAG). Unfortunately, despite Nigeria’s natural gas potential, supported by Ghana’s recent discoveries, this project is struggling to supply gas to the other countries that have signed the GAO treaty, namely Nigeria, Benin, Togo and Ghana and the question of natural gas supply for the production of electricity is acutely important in these countries.

This project is in the process of being merged into the framework of the Atlantic African Gas Pipeline Project (AAGP) which will be the merger of the West African Gas Pipeline Extension Project (WAGPEP) and the Nigeria-Morocco Gas Pipeline Project (NMGP) into a Single Sub-Regional Gas Pipeline Project that will cross thirteen (12) West African countries and Morocco to finally serve the European market.

This means that this Nigeria-Morocco gas pipeline initiative, although commendable, deserves to be re-examined through the evaluation of the commitments of the various parties and the definition of a more unifying project policy and governance body that will guarantee the production, sale and purchase of natural gas first and foremost for our needs in West Africa. and subsequently in Africa in general, before considering supplying gas to markets outside Africa. It is important to mature this African Atlantic Gas Pipeline Project (AAGP) in order to prevent it from simply not being used to make Morocco a hub for the transit and supply of natural gas to Europe to the detriment of the ever-growing needs of Africa in general and sub-Saharan Africa in particular.

1.4.2- At the level of the APPO

At the continental level, the African Petroleum Producers Organization (APPO), which is a specialized institution created in 1987, has struggled to find its feet and remains today an organization with no significant impact on the development of oil activities in Africa. This noble initiative of the founding fathers (Algeria, Angola, Benin, Cameroon, Congo, Gabon, Libya, Nigeria), was born from the observation that, despite the abundance of hydrocarbon resources on the continent, African countries remain largely dependent on foreign multinationals for the exploration, exploitation and marketing of their oil. The fundamental objective of the APPO was therefore to promote technical cooperation between member states in order to strengthen their control over their oil resources and maximize the benefits derived from their exploitation for the socio-economic development of their populations. In more than 30 years of existence, no viable structuring project has been carried out under the aegis of the APPO through its bodies.

This organization also deserves to be rethought through the redefinition of its objectives and bodies in order to be more operational to solve the problems listed above faced by the different segments of the value chain of the hydrocarbon sector in Africa.

- Possible solutions for an oil industry serving the region

The need for a reorganization of the entire value chain is a solution to boost development in Africa. This reorganization involves:

-

the establishment of a structure and an endogenous financing strategy for oil exploration and production projects;

-

the development of petroleum infrastructure for the storage and transport of hydrocarbons. The establishment of such an infrastructure network will facilitate the supply of hydrocarbons in the different regions of Africa;

-

the realization of common energy structuring projects allowing the production of energy for the benefit of African populations, more than half of whom do not yet have energy. These projects will enable the development of the entire value chain of the hydrocarbon sector

-

the construction of regional refineries in accordance with environmental standards in the current context of climate change and related infrastructure;

-

the creation of specialized training centers for petroleum professions;

-

the development of healthy cooperation between States in terms of sharing experience.

Figure 4: Synthetic diagram showing the different oil cuts

0 to 80-100°C

120 to 180°C

Chapter 2: Different Phases of Upstream Oil and the Roles of States

The Upstream Oil sector includes five (05) categories of activities or phases that follow one another (Figure 5): Pre-licence, Exploration, Development, Production and Abandonment.

Figure 5: Different phases of upstream oil

Authorization to operate

Exploration Authorization

- Pre-licensing phase

2.1.1- Definition of the concept

During this phase, the State puts in place the policy as well as the regulatory and technical tools necessary for oil exploration, promotion, allocation of oil blocks, management and monitoring of contracts/authorizations or licenses as well as environmental management related to the realization of oil exploration and exploitation activities.

The pre-bachelor’s degree stage addresses, among other things, aspects relating to:

-

preliminary geological and geophysical reconnaissance or prospecting studies (gravimetry, magnetometry, speculative seismic, etc.), the objective of which is to define the areas suitable for exploration and to assess their oil potential;

-

the establishment of laws and regulations that should clarify the main areas of concern for both the investor(s) and the host government. This will enable the host Government to ensure better monitoring and proper management of contracts and to effectively monitor revenue forecasts through the establishment of an appropriate and mutually beneficial tax and legal regime.

-

the delimitation of maritime and land borders as well as the mechanism for managing border conflicts in oil zones common to two or more States;

-

the management of the involvement of local communities and the expectations of the populations.

Once the areas potentially favourable to oil exploration have been known and the oil potential assessed, the technical and environmental laws and regulations and the tools for awarding and managing oil contracts have been developed, States can proceed to allocate perimeters for exploration.

The issuance of a petroleum licence or authorization follows the process outlined in Figure 4 below. It starts with promotional activities until a contract is signed and/or an authorization is issued that gives the IPCs the right to explore and exploit hydrocarbons in a well-defined area commonly known as an oil block.

- Strategy for awarding petroleum licences or authorizations

Promotion is the operation of attracting investors in oil exploration and exploitation. Countries with oil potential and wishing to embark on the development of their oil resources must prepare and/or regularly update petroleum promotion documents. A promotion file must contain the following documents:

-

Petroleum legislation

-

The contract model

-

The list and price of available oil data if required. Some countries make data available to oil companies free of charge to be more attractive

-

Information on the oil potential and/or a technical assessment report of the oil potential

-

Perimeters or blocks on promotion

-

Information on available oil infrastructure

-

The institutional framework of the hydrocarbon sector and contacts of the structures in charge of this sector

-

The Tender Calendar

-

Pre-qualification criteria

-

Evaluation criteria

The different stages of the allocation of oil blocks are (Figure 6):

-

Announcement of the exploration area or blocks on promotion

-

Launch of the call for tenders: the launch of a call for tenders makes it possible to have several offers on the same domain or block; this makes it possible to make comparisons in order to choose the most interesting offers for the State. However, it is not excluded that the State will decide to examine, on the basis of its expectations, the unsolicited offers of companies that show an interest in a given block.

-

The definition of the pre-qualification criteria: the pre-qualification constitutes a first filter of the oil companies on the basis of criteria previously defined by the States in order to identify the oil companies or consortium capable of playing a relevant role in the field where the blocks are auctioned; These criteria generally relate to the financial, technical, security and environmental management capacities of oil companies

-

Submission of tenders: this consists of the submission of applications by oil companies that are interested in oil exploration in the fields open to tendering

-

Analysis/evaluation of tenders: this is done on the basis of the award criteria developed by the Government.

-

Allocation of the block: this is done after negotiation of the technical and economic terms with the CPIs who present the best offers on the basis of the State’s expectations. The technical and fiscal terms that may be subject to negotiation and that condition the final allocation are:

-

Work obligations

-

Retrocession or surface rendering

-

Local Content and Training

-

Socio-community development

-

Signing and Exploitation Bonuses

-

Royalties

-

State participation,

-

The cost stop rate

-

The key to sharing oil profit, etc.

-

Oil negotiations require good preparation and professionalism on the part of the Government. It is carried out by a multidisciplinary team which must include, but is not limited to, players with a good knowledge of oil contracts and negotiation techniques as well as technicians experienced in the sector. This team can be made up of lawyers, oil economists, geoscientists, etc.

Figure 6: Process for Assigning Oil Block to the IPC for Petroleum Exploration and Development

All in all, pre-licensing activities are necessary because they condition the decision of governments whether or not to engage in oil exploration activities.

This was the beginning of investments in the hydrocarbon sector.

- Financing of pre-licensing phase investments

As a general rule, pre-licensing activities are under the sovereignty of the host state. The implementation of policy documents, legislation and regulations, as well as the assessment of oil potential and the implementation of tools and strategies to move to exploration via international oil companies are the responsibility of States and require relatively less expensive investments than those relating to exploration activities. States with financial resources and competences directly finance all these activities (Norway for example). However, those with limited financial resources and no required skills are accompanied for certain pre-licensing activities by service companies to carry out the first reconnaissance and evaluation studies of the oil potential in order to have first-hand information before engaging in promotional activities that lead to the signing of exploration and exploitation contracts with oil companies. These service companies usually acquire the data at their own expense on the basis of a service contract and market and market it to international oil companies.

- Importance of the pre-licensing phase and responsibilities of the State

The pre-licensing phase is very essential in the sense that the lack of knowledge of its oil potential and the non-existence from the outset of all the clear regulations, procedures and tools for the management of upstream oil activities are detrimental to the signing of fair and beneficial contracts for the State.

“You can never sell a packaged good at its fair value, i.e. very little or poorly known .”

The non-or poor preparation of the pre-licensing phase thus leads to harmful consequences for States during the execution of oil operations, where they are confronted with legal and contract management difficulties.

Unfortunately, most African countries neglect this phase and engage in the exploration and exploitation of oil resources without any necessary safeguards by signing contracts whose revenue sharing is often unfavorable or very unprofitable following the discoveries. The lack or inadequacy of proper preparation for the pre-licensing phase, which is essential for the implementation of tools for managing and monitoring contracts before engaging in oil activities (which contributes to the development of resources), is often one of the fundamental causes of the signing of “one-sided contracts” with foreign partners in the geo-extractive sector in general and in the oil industry in particular in Africa.

- Exploration phase

2.2.1- Exploration methods and strategies

Exploration is the phase of upstream oil activities that consists of the search for hydrocarbons in the subsoil using geological and geophysical methods, including seismic methods, and the drilling of exploratory wells. Initially, the research consisted of drilling near natural surface showings; This only made it possible to discover small deposits, close to the surface.

Today, it is undertaken by the International Oil Companies (IPC) which have developed several exploration methods and technologies from the simplest to the most sophisticated for the discovery of hydrocarbons at great depths both on land and in very deep seas (beyond 3 km of bathymetry).

The activities concerned by the exploration are, among others:

-

Surface geological research

-

Gravimetry,

-

Magnetometry

-

Aerial photography

-

Seismic

-

Electromagnetism (EM) or Control Source Electro-Magnetic (CSEM)

-

Exploration drilling

Gravimetry and magnetometry help to identify areas of geophysical anomalies where other, more precise methods can be applied to locate hydrocarbons. They make it possible to determine the nature and depth of the sedimentary layers and thus give an idea of the distribution and thickness of the sedimentary formations (Figure 7 a and b).

Figure 7: Gravimetric acquisition (a) showing anomalies in the Coastal Sedimentary Basin of Benin (CGG 2013) and aeromagnetic (b) to characterize the basement and sedimentary formations

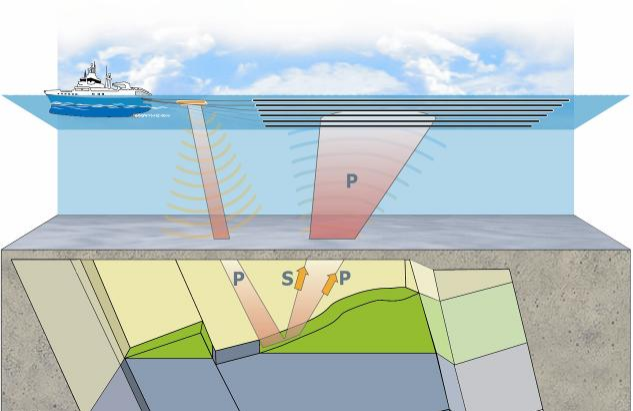

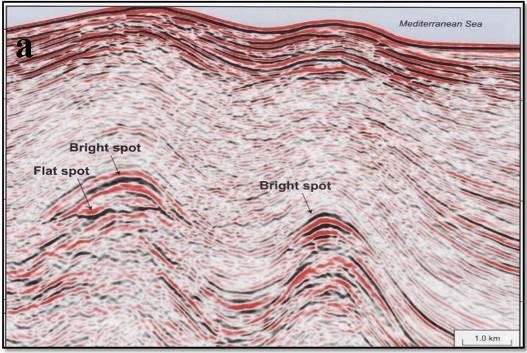

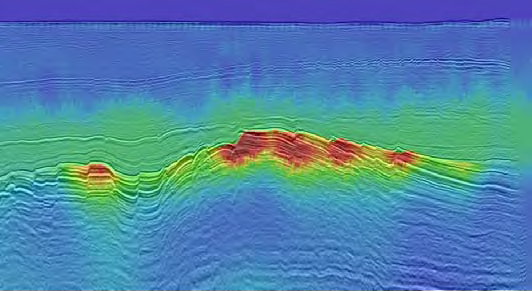

Seismic reflection, the most commonly used method before exploratory drilling. The principle of seismic acquisition consists of sending sound waves into the ground that are reflected by the different rock surfaces. The time taken by the waves to come to the surface and to be recorded by geophones (when the operation takes place on land) or hydrophones (when the operation takes place at sea) indicates the depth of the rocks crossed (Figure 8a, b). Seismics can be carried out in two 2D dimensions and for more than half a century in three 3D and even four 4D dimensions. Seismic also provides information on the nature of the rocks from the analysis of the different transmission speeds noted at the level of the different types of rocks. The analysis and interpretation of seismic data also allows the identification of hydrocarbon traps and Direct Hydrocarbon Indicators (HIDs) such as Bright Spots, Flat Spots and Gas chimneys etc. which condition the positioning of exploration wells (Figure 9).

b

a

Multiple qv streamers

Source

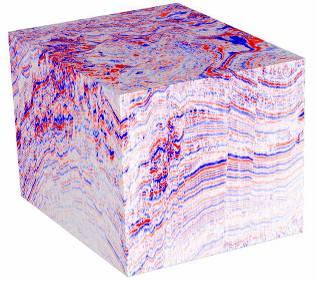

Figure 8: 3D acquisition principle (a) and seismic cube (b)

Well Positioning

Exploratory

Figure 9: Seismic amplitude anomalies showing Brightspots and Flatspots

CSEM is a technology developed that measures resistivity contrast in the seabed. The acquisition of EM is generally done on the prospects/traps already identified by the seismic in order to have a precision on the nature of the fluid contained in the traps. Indeed, the areas of oil traps have a high resistivity while the rocks around the traps are conductive because they generally contain salt water (Figure 10). This technology makes it possible to determine whether or not there is a resistivity contrast in regions where traps have been mapped in order to maximize the chances of success of exploratory wells.

Positioning an exploratory well

Figure 10: Electromagnetism coupled with seismic reflection showing the contrast of resistivity at the level of the traps highlighted by the seismic

Exploratory drilling is the ultimate and very expensive step in exploration that makes it possible to confirm or refute the predictions of exploration geologists and geophysicists.

The duration of an exploration license varies from 7 to 9 years in West African countries.

2.2.2- Techniques for evaluating a prospect

Oil exploration is based on four fundamental principles, namely: the search for the existence of a petroleum system in the licensed area by the various research methods mentioned above, the identification and mapping of geological structures likely to contain hydrocarbons (Plays, leads and prospects), the assessment of the geological risks associated with the mapped structures and finally the volumetric estimation of the potential for petroleum resources.

- Petroleum system

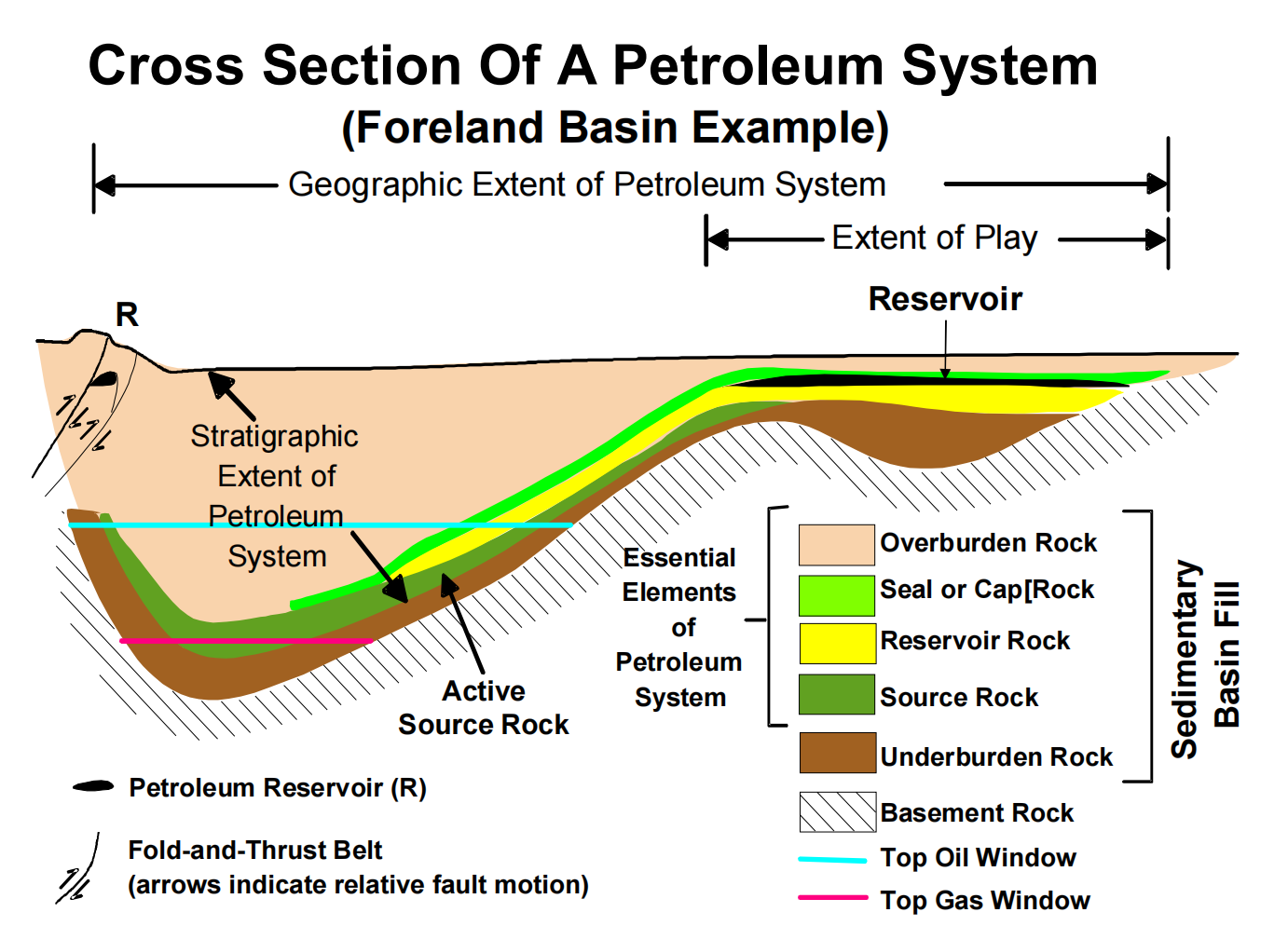

The petroleum system is the whole of source rocks, reservoir rocks, cover rocks and overload rocks as well as the entire process of trap formation, generation, migration, accumulation and preservation hydrocarbons (Figures 11 and 12). These essential geological factors and process must take place in time and space so that the organic matter contained in the source rock can turn into an accumulation of oil (Magoon & Dow, 1994).

It should be noted that this organic matter from which oil was formed, several million years ago, is the result of the decomposition, under the effect of sedimentary subsidence pressure and geothermal temperature, of microscopic animals and plants (phytoplankton and zooplankton) that lived in the sea.

Figure 11: Geological section showing the stratigraphic extent of a fictitious petroleum system (Magoon and Dow, 1994, modified by Schlumberger)

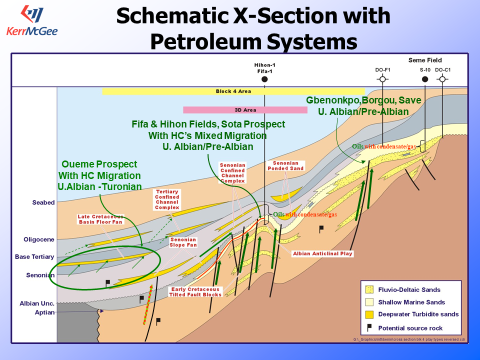

Figure 12: Geoseismic section showing petroleum systems in the Benin Coastal Sedimentary Basin, Kerr McGee, 2003

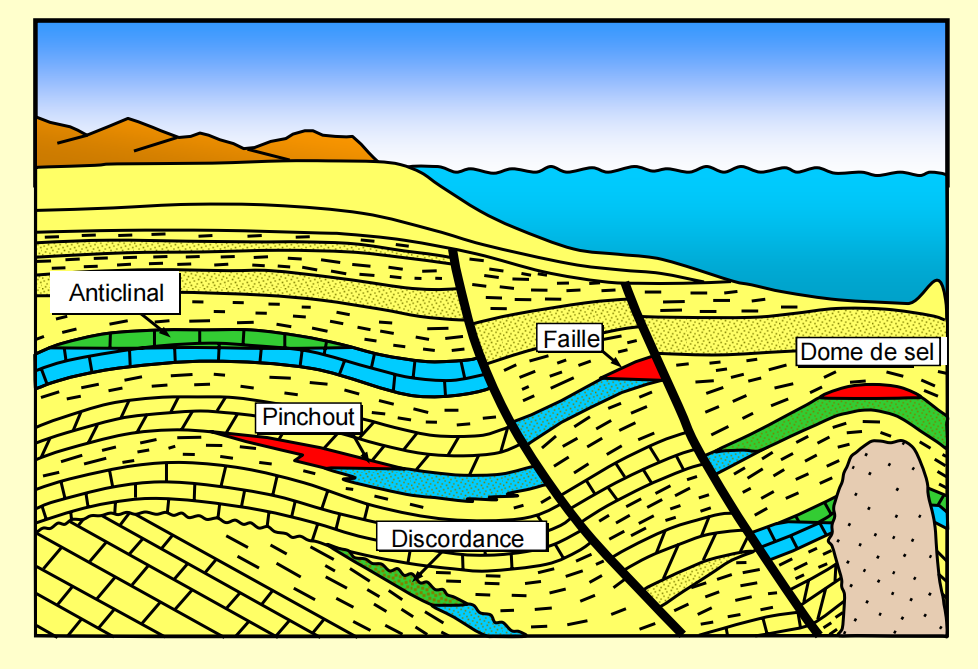

- Identification and mapping of geological traps likely to contain hydrocarbons

Geophysicists and geologists process and interpret the data acquired by the various research methods in order to identify hydrocarbon traps (Figure 13), HIDs or any other geological anomalies that make it possible to suspect the presence of hydrocarbons and that make it possible to guide the positioning of exploratory wells.

Hydrocarbon traps can be structural, stratigraphic or mixed depending on their formation mechanism.

Structural traps can be formed by regional tectonic mechanisms (fault, anticline, etc.) or by salt tectonics (halokinesis). Stratigraphic traps result from depositional conditions, i.e. are formed by sedimentary processes (unconformity, lateral change of facies, bevel, etc.) (Figure 14).

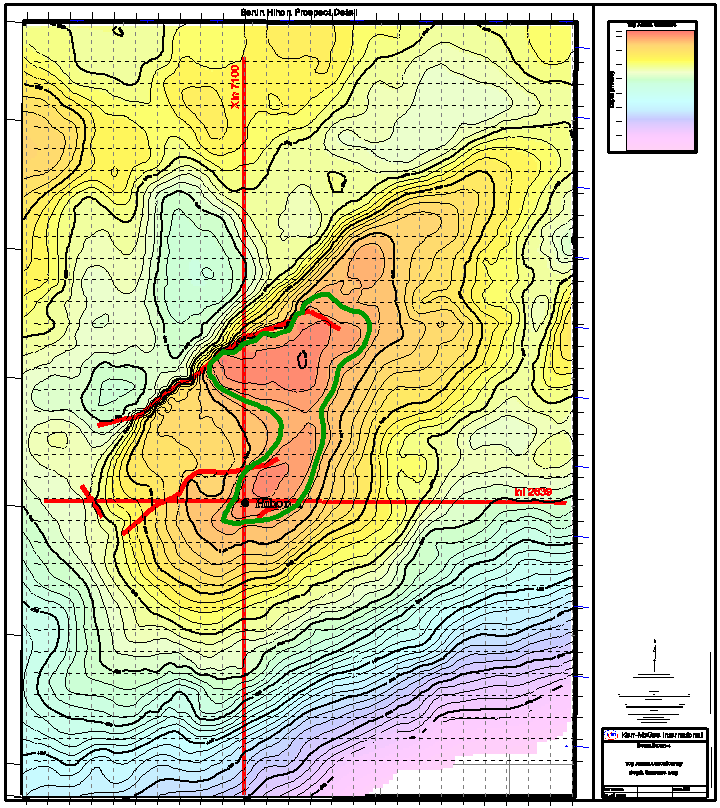

The identified traps are then mapped using software in order to assess their geometry and assess their size (Figure 15).

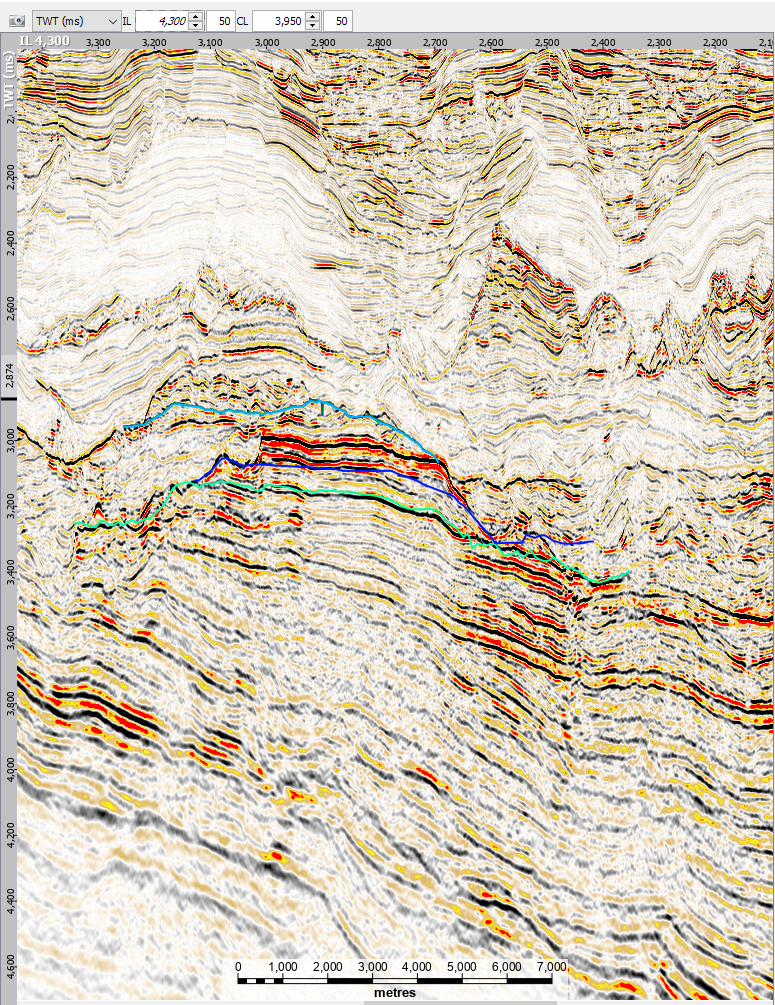

Figure 13: Seismic interpretation showing a structural trap (anticline)

Figure 14: Some types of traps

Figure 15: Depth map showing the roof of a tank

- Geological risk assessment

Geological hazard assessment is used to determine the probability of success of exploratory drilling on a mapped prospect. The assessment of the geological chances of success associated with a prospect is done by assigning probabilities to the key geological factors that are essential to the formation and preservation of an oil or natural gas accumulation.

Thus, the determination of the geological risk of a prospect makes it possible to calculate the probability of success of this prospect. It is determined by the formula:

P(prospect) = P(source rock) x P(reservoir) x P(trap)

Waterproof trap + waterproof cover

Porosity and permeability of reservoir rock

Geological hazards

Maturity of the bedrock and therefore its degree of migration to the reservoir

(iv) Volumetric assessment of hydrocarbon resources

The evaluation of the hydrocarbon resources contained in the prospect consists of estimating the volume of oil or natural gas that could be found in the prospect. It is carried out using the geological and petrophysical parameters of the reservoir rock. This assessment is more accurate when using the results of the work carried out, in particular the results of exploratory drilling. Failing this, the parameters from the seismic interpretation or from the wells adjacent to the research area are used.

Thus, the quantity of hydrocarbons (VHcP) in place, i.e. oil (STOIIP) or gas (GIIP) in place, is determined as follows:

VHcP = GRV x N/G x Ø x Shc x 1/FVF

With

IBC = Gross Rock Volume: it is determined by taking into account the geometric shape of the reservoir and its thickness

IBCs = ∑Deposit Area x Deposit Thickness

N/G: This is the ratio between the net thickness of the tank and the gross thickness of the tank. It should be noted that the thickness of the deposit does not often have a uniform lithology. It is often interspersed with layers of impermeable clay.

Ø (Phi) = Reservoir porosity which is estimated from electrical logs, core measurements and knowledge from similar formations. It is determined as follows:

Porosity (Ø) = Pore Volume (Vv)/ Reservoir Volume (V)

Shc = Hydrocarbon saturation determined by knowing the water saturation Sw. It is usually calculated from the well digraphies in the effective porosity zone.

Shc = 1-Sw

FVF: This is the Volumetric Factor of Formation. It expresses the change in the volume of the oil from the tank to the surface under standard pressure and temperature conditions (pressure: 1 atm and temperature: 15° Celsius). FVF of the oil is Bo and for the gas is Bg.

FVF = Reservoir Volume/Surface Volume

- For the oil

FVF = Bo and Shc = So (oil saturation)

Thus,

STIIOP = GRV x N/G x Ø x So x 1/Bo

Associated gas in place = STOIIP x GOR

- For gas

FVF = Bg and Shc = Sg (Gas Saturation)

Thus,

GIIP = GRV x N/G x Ø x Sg x 1/Bg

Condensate in place = GIIP x CGR

with:

GOR: called Gas-Oil Ratio is the ratio of gas volume to oil produced

CGR: called Condensate-Gas Ratio is the ratio of condensate volume to the volume of gas produced

A lead ranking is performed when multiple leads are mapped on a contracted block. This classification is based on geological hazards (probability of success), the volume and type of hydrocarbons potentially in place, and other petrophysical parameters. The choice of the prospect(s) to be drilled takes this ranking into account in order to maximize the chances of success.

Once a discovery is made, the ICC carries out the work to evaluate the deposit. This work includes a set of activities, namely the drilling of appraisal or delineation wells, geological and geophysical studies of reservoirs as well as an evaluation of reserves to decide on the development of the deposit when it is commercially exploitable.

- Financing of exploration activities

Exploration activities are almost entirely funded by the IPCs as states lack the financial resources, technology, human skills and operational capacity to engage in this high-risk project.

Oil exploration is the most delicate phase with high risk in the sense that it involves heavy capital investments (CAPEX) for results whose probability of success is generally below the global average. Despite technological advances in oil exploration, the failure rate is high. About 2/3 of the exploration wells are dry. In the absence of commercial discovery during the exploration period, the CPIs lose all their investments.

- Responsibilities of States in the exploration phase

During this phase, the host country, although it does not often take financial risks, has a great responsibility vis-à-vis the contracting CPIs who assume virtually all the risks associated with the investment capital.

The two most essential roles of the State, owner of potential resources, are: the establishment of an oil database and the monitoring and technical and financial control of all activities carried out by the contractor.

- Oil Data Management

The host country must ensure the collection and preservation of all oil data acquired during this phase. These oil data constitute a decisive basis for future investigations. They have significant scientific and economic value in the sense that they provide information on the geology and resource potential in the subsoil of states.

This data concerns those produced during the exploration phase but also those generated during the development, production and abandonment phases. Some countries, due to a lack of means of conservation, i.e. technical and infrastructural capacity, entrust the storage and management of their data to partners or specialized foreign companies outside their territory. In doing so, they behave like landlords who entrust the key to their safe to their tenants.

“By entrusting the management of oil data to specialized foreign companies, states no longer have enough control over the various manipulations and businesses to which they are subjected. As they do not have control and management tools, they are unaware of the quantity and quality of their data, and consequently the economic value of their assets”.

They are therefore required to believe in the balance sheets and evaluations as well as in the decisions and choices of oil companies in the context of the implementation of oil operations.

This is why it is necessary for States to create adequate storage and conservation centers as well as laboratories for quality control and analysis of acquired oil data, which, in the same way as oil resources, constitute State assets. To this end, it is essential for States to adopt a real policy for the control and management of their oil data. Some West African countries are aware of this and are developing a good data conservation, analysis and management strategy. Côte d’Ivoire and Nigeria are a good example of the establishment of a centre for adequate storage and preservation and data analysis (Figure 16).

Figure 16: Photos showing the core library of Côte d’Ivoire at the Direction of the PETROCI Analysis and Research Center

- Monitoring and control of activities

The regulation of exploration activities includes not only the monitoring of the implementation of contractual obligations but also the control of the costs of carrying out activities as well as compliance with standards and procedures for the execution of activities in accordance with national regulations or those of the international oil industry. The monitoring and technical control of activities are fundamental sovereign functions of the State that require the existence of qualified human resources and the implementation of effective control tools for oil and exploration operations, including the management of environmental risks and impacts related to the implementation of these activities. This monitoring must be regular and well planned insofar as it is at this level that the contractor, driven by the search for maximum profit, could take advantage of the failure of the State’s control and audit mechanism to overestimate exploration costs or even deviate from the best practices of environmental protection during the implementation of activities.

In short, it is the responsibility of the States to monitor the effectiveness of the implementation of the activities reported, the optimal deadlines for completion, the quality of the work carried out at the technical level and in compliance with the environmental standards accepted or prescribed by the regulations and to audit the actual costs of their implementation through the development of a directory of the costs of the activities. This directory will have to be updated to serve as a reference for confrontations and audits.

- Development Phase

2.3.1- Definition and strategies

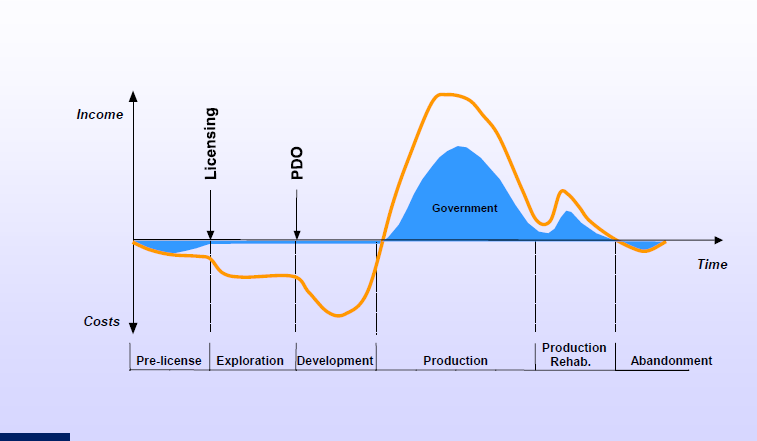

The development of an oil field consists of carrying out operations that contribute to the establishment of the production infrastructure of the discovered field(s). These typically include production platforms, production drilling, and infrastructure for storing and transporting crude oil or natural gas from the wellhead to the point of delivery, and onshore or offshore effluent collection and treatment facilities. During this phase, geological assessment studies, reservoir evaluation, feasibility studies and FEED (Front and End Engineering Design) studies are carried out in order to choose the best development option from a technical, economic and social point of view. All these studies contribute to the elaboration of a Development and Operation Plan (PDO) which is a clear document that describes the feasibility of the development project in its various well-planned aspects.

The PDP includes:

-

Geological assessment

-

Reservoir evaluation and reservoir technology including secondary and tertiary recovery study

-

Production and Drilling Technology

-

Facilities

-

Equipment maintenance

-

Economic evaluation

-

Safety and Environment

-

Project organization and execution

-

Abandonment plan

From discovery to production, it takes an average of three to four years for the development of an oil field. This means that this phase is very delicate in the sense that the optimal exploitation of a deposit depends on the development model chosen.

The choice of a development model depends on several technical and economic parameters, including the existing facilities or those to be set up, the nature or type of the reservoir (single or multilayered) and the thickness of the reservoir, the location of the reservoir (onshore, deep or shallow offshore), the quality of the reservoir, the quality of the crude oil and its market price, etc.

2.3.2- Reservoir Evaluation Methodology

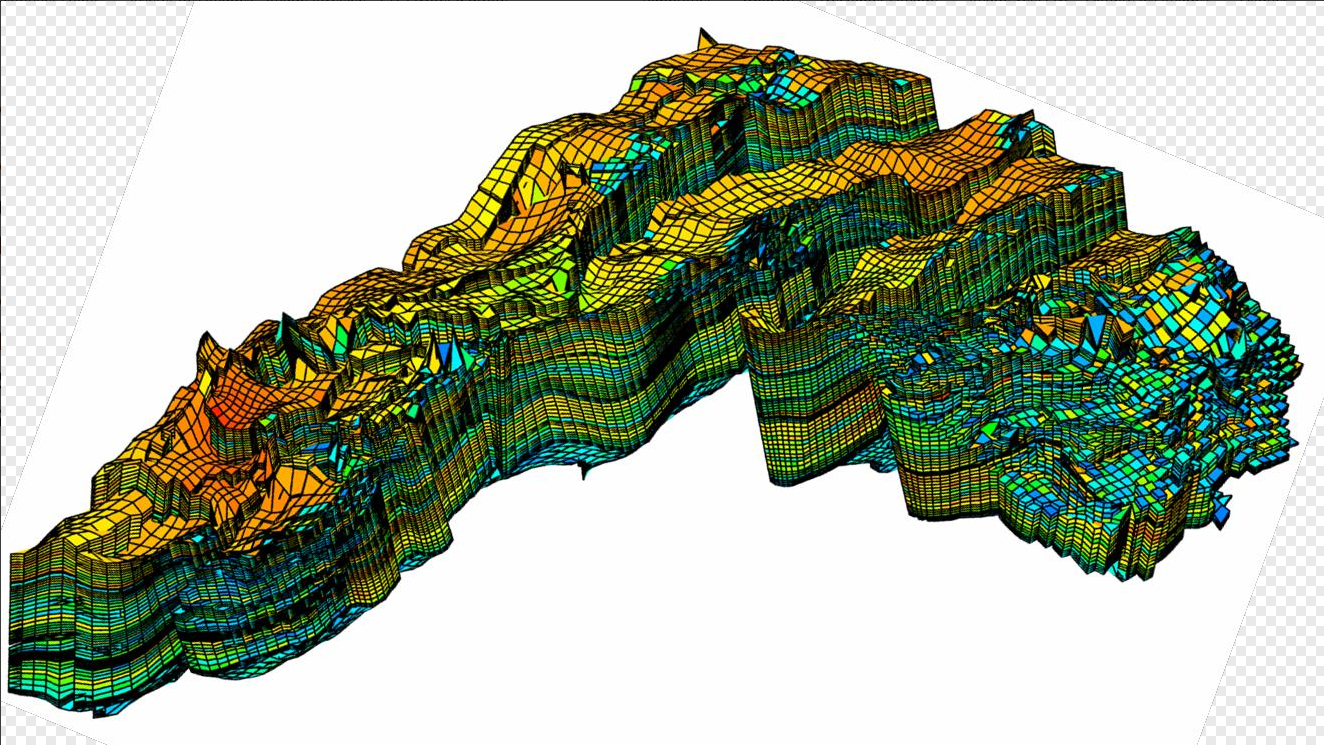

The reservoir assessment is carried out according to the methodology shown in Figure 17 below. This methodology starts from data collection to the economic evaluation of the deposit. It allows, after processing, interpretation of the data, i) to carry out the modelling/simulation of the reservoir on the basis of the data available on the reservoir, i.e. seismic data, well logs, cores, well tests, ii) to determine the performance of the reservoir and iii) to project the most optimal and responsible production profile as well as the economic profitability of the development project with a view to decision-making of the deposit.

Geological and reservoir simulation studies provide detailed models of underground reservoirs to predict their behavior over time through the calculation of fluid flow fluxes that are a function of reservoir properties and well conditions (Figure 17). Simulation is therefore an essential decision-making tool that allows:

-

optimize production through i) a better understanding of the most efficient means of hydrocarbon recovery, i.e. the different recovery methods adapted to the characteristics of the reservoir (reservoir with active aquifer, reservoir with cap gas, the lithological nature and thickness of the reservoir, etc.), ii) the number and types of wells (vertical, inclined or horizontal) adapted to the reservoir in order to maintain its performance ;

-

manage risks by assessing and mitigating risks associated with drilling and production

-

to make an economic planning or forecast to help in an investment decision.

Excavated material, cores, seismic data, logging, well tests, etc.

RAW DATA COLLECTION

Descriptive elements of the reservoir (porosity, permeability, water saturation, pressure, oil viscosity, etc.)

PROCESSING AND INTERPRETATION OF THE DATA COLLECTED

INTEGRATION AND

MODELING

Tank Models and Understanding of the Tank

EVALUATION DES OPTIONS DE RECUPERATION

-

Recovery Methods (Primary, Secondary, and Tertiary)

-

Types/types of wells (production, injection and observation/horizontal, vertical, inclined, etc.)

-

Etc

Tank Performance Prediction

CAPEX, OPEX, Risk

ECONOMIC EVALUATION AND DECISIONS

Figure 17: Methodology Tank Evaluation

Figure 18: Diagram showing a reservoir model (Vilgeir Dalen, StatoilHydro, 2007)

2.3.3- Financing of development activities

Development involves large capital expenditures (CAPEX) in the upstream oil subsector. Enormous financial resources are invested in the production of hydrocarbon deposits. It should be noted, however, that the risk is lower during this phase compared to the exploration phase; The question that arises is no longer the doubt about the existence of the deposit, but it is above all that linked to the benefit/cost ratio of investments, which is a function of the technical and economic parameters and conditions related to its exploitation. This is why, before embarking on development operations, several preliminary profitability studies are carried out and recorded in the PDO submitted to the State for approval.

2.3.4- Roles and responsibilities of States in the development phase and Relevance of a PDO

The development of an oil field is subject to the approval by the Government of a Development and Operation Plan (PDO) or a feasibility study drawn up by the contractor and submitted to the State. The PDP preparation and approval process provides opportunities for dialogue between the contracting company and the host state on how the field should be developed and produced in a sustainable manner so that both parties can benefit the most. Thus, before the approval of the PDO, the State must proceed:

- The geoscience assessment of the PDP , which aims to:

-

Ensure that the quality of the reservoir interpretation is convincing enough for a development decision

-

Agree with the ICC on the PDP’s findings before it is approved

To this end, it is recommended that States:

-

Conduct in-house studies and interpretations based on well data, seismic data including 3D and VSP, maps etc.

-

certify the assessment of recoverable reserves and the feasibility study by its specialists or a third party

-

to organise meetings and dialogues with the operating company on the basis of the results of the counter-expertise work carried out by the State for fruitful technical exchanges

- The evaluation of the reservoir which aims to**:**

-

Ensure an optimal production strategy selection

-

Define the use of gas in an oil field

-

Ensuring the possibility of oil recovery in a gas field

-

define and guarantee the implementation of a serious and responsible production profile

-

Ensure proper management of the tank

-

Ensure consistency (correlation) between geology, reservoir and production strategy.

In short, the State, as the owner of resources, must:

-

avoid the hasty start of hydrocarbon development operations. Any start of the development plan must require the approval of the State after examination of all the preliminary studies and documents required by the petroleum legislation, including the reservoir simulations.

-